A write-down is the cost a board can see. The larger cost arrives over the next two years, and most boards never price it.

When a governance failure reaches the share price, the board sizes the damage at the moment of the event and adds up the fall, the fine, the settlement and the impairment. That figure understates the true cost by a wide margin, because most of it accrues over the two years that follow.

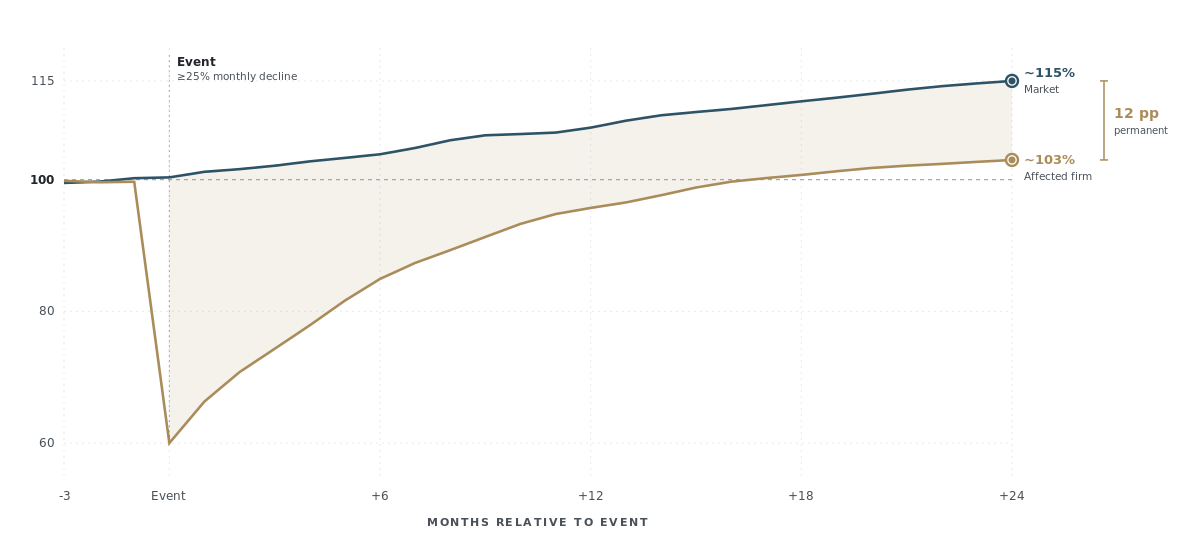

The number boards miss

Stefan Hunziker and colleagues examined 669 listed firms across Germany, Austria and Switzerland between 2018 and 2024. They isolated the firms that suffered a severe crisis, defined as a monthly share-price decline of 25% or more, and tracked each one against the broader market for the 24 months that followed.

Two years on, the average affected firm had returned to roughly 103% of its pre-crisis value, slightly above where it started.

Over the same 24 months, the broader market advanced to about 115%. The affected firm spent two years climbing back to its starting point while the market compounded the growth the firm could not capture. The gap between the two, roughly twelve percentage points, persists.

That gap is permanent loss of relative market position. The firm regains the visible fall, then settles below the level the market has since reached. The interactive version of this chart lets you drag a scrubber across the full 24-month window and watch the gap open month by month. The write-down is sharp and visible; the gap is slow and permanent.

Why the gap does not close

The write-down triggers the damage. An amplification chain makes it durable.

The first link sits in the share price itself. Total shareholder returns over the 120 working days after a disclosure event were affected at more than twelve times the direct monetary loss from fines, settlements and remediation (McKinsey, via Grimwade, 2025). The market reprices the firm’s prospects, far beyond the cash cost of the event itself.

The second link sits in the cost of capital. A one-notch credit downgrade typically widens debt spreads by 10 to 50 basis points, and the recovery is slow. After its 2011 rogue-trader incident, UBS took five years to return its Fitch rating to ‘A’, and a further fifteen months to reach ‘AA-‘. For that entire period the firm funded itself at a premium its competitors did not pay.

The third link sits in the client base. In the fourth quarter of 2022, Credit Suisse clients withdrew CHF 138 billion in deposits, and wealth and asset management recorded a further CHF 111 billion in net outflows over the same quarter. The outflow outran the rescue. Each link feeds the next, and the damage migrates from the share price into the operating posture of the company: higher funding costs, a smaller franchise, and decisions taken under constraints that did not exist before the event.

A structural signature, not a local result

A board might reasonably treat one dataset as an artefact of its period or its region. The recovery gap survives that objection.

Hunziker and colleagues replicate a 1998 Mercer Management Consulting study of the US Fortune 1000. Two independent datasets, separated by twenty-seven years and an ocean, produce the same pattern. Affected firms recover the visible loss, then underperform the market for years. The gap describes what a severe governance failure does to a firm’s relative position, in any market and any decade.

Price governance against the gap, not the event

Most boards size their governance investment against the write-down they can picture, the fine, the settlement, the headline loss. Priced that way, continuous independent challenge looks expensive against a risk that may never arrive.

Priced against the gap, the arithmetic inverts. The cost of a governance failure is the write-down, plus two years and more of missed market participation, plus relative underperformance that, on the evidence, endures. Governance that prevents the event earns its cost against that full figure. The visible write-down is only a fraction of it.

That is the case for governance that is continuous rather than episodic, independent rather than consensual, and adversarial by design, a standing capacity to interrogate the assumptions behind a decision before it is made. Its value is measured against the gap the event leaves behind, which is where the largest cost has been all along.

From the SGaaS White Paper

The full evidence and the structural response

The recovery gap is one of three empirical anchors the white paper uses to reframe governance as a continuous, adversarial investment measured against the gap rather than against the event itself.

Owen Vallis is the founder of Marentis Labs, the firm that originated Strategic Governance as a Service. He spent ten years as UK Head of Fiduciary Risk Management at Credit Suisse and holds active board roles in the public and charity sectors. Schedule a confidential discussion.